One Metro, Sixteen Markets

What Cleveland's 3.0% metro average hides: sixteen submarkets, from North Collinwood's +11% to South Collinwood's −1.3%.

Cleveland-Akron multifamily rents grew 3.0% over the past year — a middling number, the kind that belongs in a market summary written to be forgotten.

It describes nothing that is actually happening on the ground. Within the city of Cleveland alone, North Collinwood rents grew 11.0% over the past year — while South Collinwood, the neighborhood that shares its name, fell 1.3%. Between those two ends sit dozens of submarkets ranging across every direction the market can move: a spread of more than a dozen points behind a headline that reads as flat. The 3.0% is the average of forces pulling hard in opposite directions, and the average is the one figure that describes none of them.

The spread is not noise, and it is not explained by the metro. It is local — and, increasingly, it is showing up in value.

The Spread Is Real — and Local

The strongest and weakest submarkets sit a few miles apart — and it isn’t outer-versus-inner.

The spread does not reduce to a tidy rule. The submarkets posting the strongest rent growth are inner neighborhoods, not far-flung suburbs — North Collinwood (+11.0%) on the near East Side, Shoreway (+9.6%) and Edgewater (+6.0%) on the near West Side. The weakest are scattered too: South Collinwood (−1.3%), Glenville (−0.7%), and pockets along the inner-ring east. Neighborhoods that share a border can sit on opposite sides of the line. What separates them is not one metro-wide force but the specific trajectory of each submarket — its occupancy, its recent deliveries, and the direction of investment around it.

That is the recurring lesson of reading a market at the submarket level rather than the metro level. The headline is built for a national audience comparing one city to another. It was never built for an owner deciding what to do with a specific property — and for that decision, the 3.0% is actively misleading. It tells an owner in North Collinwood the market is flat when it grew eleven points; it tells an investor that Cleveland is unremarkable when the detail shows real strength and real softness a few miles apart.

The Spread Becomes a Value Spread

What rent does to net operating income, it eventually does to price.

Rent growth and occupancy are what underwrite net operating income, and net operating income is what sets value. So, the submarket rent spread does not stay a rent story. With a lag, it becomes a value story — visible in what these assets are worth and what they trade for.

Where Demand Is Being Rebuilt

The corridor’s rents are modest. Its demand trajectory is not.

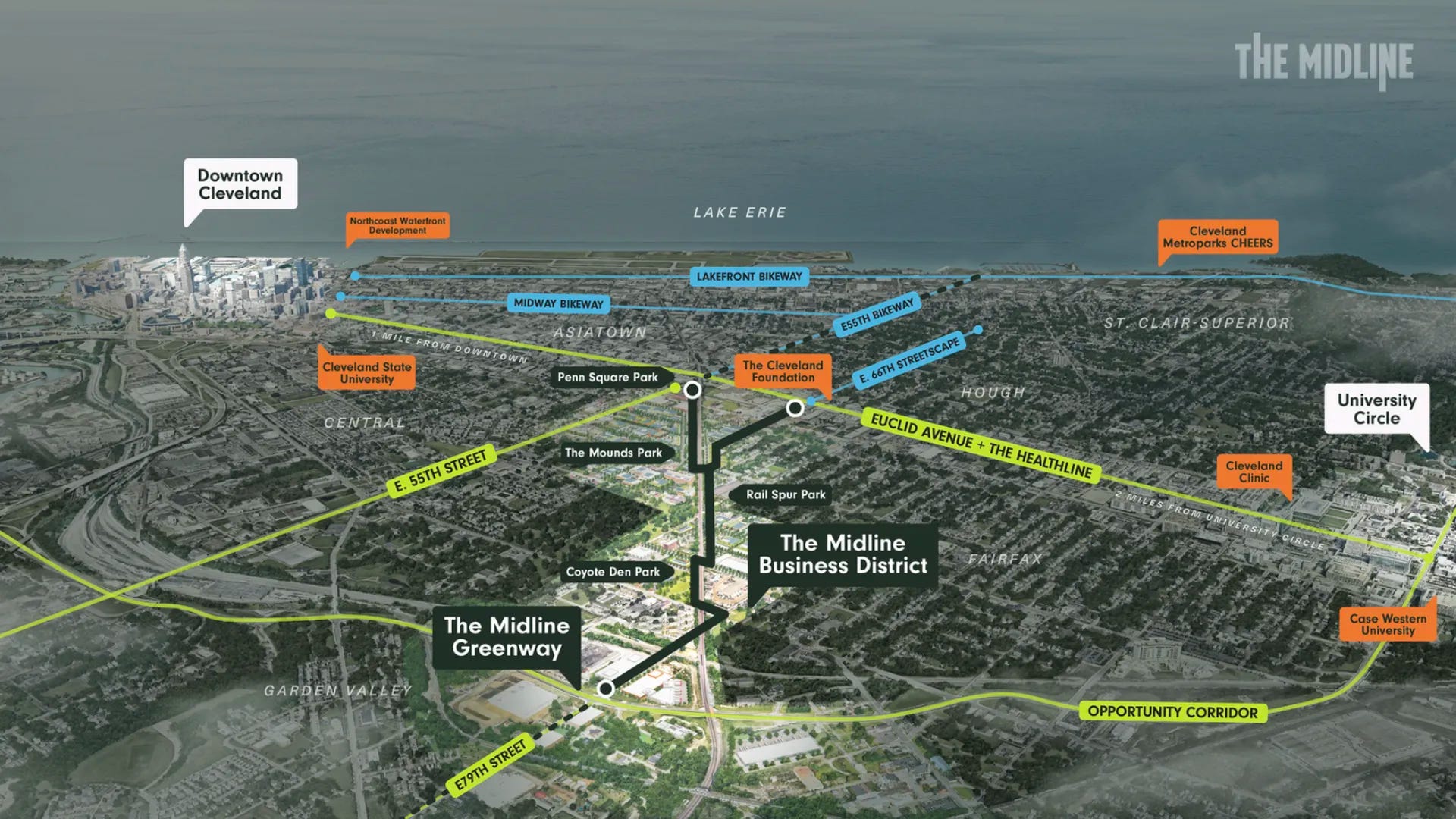

The transaction data is starting to show it, and the clearest place to watch is the corridor this series has been tracking — Hough, Fairfax, Kinsman, and University Circle, the East Side neighborhoods the Opportunity Corridor reconnected to the city’s economic core.

The corridor’s own rent growth has been modest — Hough up 3.2%, Fairfax barely above zero — middling within the spread, not leading it. So why watch it? Because what is changing there is not this year’s rent; it is the demand underneath it.

The answer is that not all supply is the same. The pipeline arriving on the East Side is arriving with demand attached. Three initiatives are converging on the same few square miles. The Midline — a 350-acre redevelopment of long-vacant near-east-side land between Downtown and University Circle — is projected to deliver more than 1.5 million square feet of commercial space, on the order of 2,500 jobs, and roughly $100 million in annual tax revenue, with some 115,000 residents within a fifteen-minute reach. In June, Cleveland City Council approved a Housing Innovation District over Hough, Central, and St. Clair-Superior, pairing a thirty-year tax-increment-financing district — projected to generate $90 to $245 million for neighborhood infrastructure — with halved multifamily permitting, waived single-family permit fees, and a form-based rezoning. The mayor’s office counts more than $368 million in transformational projects already underway across the corridor and frames the effort explicitly as housing policy joined to industrial policy.

Here is the distinction that matters. New supply that arrives on its own competes for a fixed pool of renters and pressures rent. Supply that arrives with jobs, infrastructure, and institutional capital behind it expands the pool faster than it fills. The East Side’s investment is deliberately the second kind — which is why the corridor’s modest current rent is less telling than the demand trajectory now being built beneath it. The mixed-income projects already completed on that logic, like Aura at Innovation Square, were the early evidence; the public capital now committed is the structural case.

What the rent data and the committed investment point to is a forward case, not a finished one: the corridor is stabilizing, and the capital now in motion is designed to lift it. Whether that reaches value is a question the transaction record will answer as more arm’s-length sales close — and the forthcoming Cleveland report tracks them.

The Decision the Metro Number Can’t Make

The metro number can’t answer the only question that matters for your property.

For an owner: your submarket’s trajectory, not the metro’s, is what bears on your rent position — and what that trajectory is doing to your asset’s value is the question behind the question. Whether the supply near you is demand-anchored or arriving alone is the difference between a tailwind and a headwind. Neither is answered by a 3.0% headline.

For an investor: the spread is the opportunity set. The submarkets moving hardest against the metro number, in both directions, are where the analysis produces something actionable — and where supply, demand, and price are moving together rather than apart.

The full picture — the five-year price-per-unit breakdown by asset class and submarket, the East Side comp set, and the supply pipeline neighborhood by neighborhood, set against where the corridor’s public investment is landing — is the subject of the forthcoming MarketRent™ Cleveland report.

If you own affordable or multifamily property in Cleveland, the question isn’t the metro average — it’s whether your submarket is a tailwind or a headwind for a sale. Clarendon Property Advisors advises owners on affordable and multifamily transactions. Request a confidential asset evaluation →

Pulse — What We're Tracking

Cleveland approves a Housing Innovation District for the East Side (Ideastream, June 1) — The city is pairing housing with jobs in the exact corridor this issue tracks; policy is now the demand story underneath the rent numbers.

Affordable supply is slowing but still near record highs (Yardi Matrix, June 2026) — Fully affordable deliveries eased to 91,841 in 2025 from a 99,558 peak in 2024 — still the second-highest on record — even as starts fell ~20% year-over-year in Q1 2026; federal tax-credit funding is propping up the affordable pipeline while market-rate construction pulls back.

House advances FY27 HUD bill with deep cuts (PHADA Advocate, June 2026) — The House Appropriations Committee moved a FY27 T-HUD bill funding HUD at $71.4B — nearly $6B (8%) below FY26 — though project-based Section 8 fares better than most accounts; the Senate hasn't acted and a continuing resolution looks likely. The federal funding backdrop every affordable owner is underwriting against.

Also tracking:

The Midline business district — the jobs-and-greenway spine the East Side thesis rests on

National multifamily rents (Yardi Matrix) — Midwest/gateway metros lead; supply-heavy Sun Belt still contracting

Mayor Bibb: “America Needs a New Housing Playbook” (Justin Bibb, Jun 3) — the mayor frames Cleveland’s housing strategy as industrial policy, in his own words

Tools • Services • Archive • About • Contact

About: Clarendon is a trusted partner for government compliance and advisory solutions, specializing in HUD-compliant services: brokerage, appraisals, rent comparability studies, market studies, inspections, facility support and strategic guidance for agencies, housing authorities and property owners nationwide.

© 2026 The Clarendon Group, Inc. All Rights Reserved. Disclosure

Submarket granularity is where the real analysis lives. It's great to see the data finally mapping this precisely.