Downtown Detroit: The Conversion Pipeline That Remade the Core

While other cities are just entering the office-to-residential era, Detroit has been doing it out of economic necessity for decades — and the downtown submarket data shows what that history produces.

This is the second article in MarketRent™’s Detroit series. The city-level overview was published in The Motor City’s Second Act. This piece covers the downtown development story specifically — the conversion pipeline, the developers behind it, and what the current submarket data shows for investors and owners evaluating downtown assets.

Detroit has been converting empty office towers into apartments for over a decade. While Manhattan, San Francisco, and Washington DC are just now writing the playbook on office-to-residential conversion, Detroit was already doing it — not as post-pandemic strategy, but out of economic necessity. The result is a downtown residential market with depth, character, and the kind of submarket data that only comes from a cycle that has already played out.

That history matters for how you read the downtown submarket data today.

A Decade of Adaptive Reuse Before It Was National Policy

Detroit’s adaptive reuse story is rooted in the same economic logic that drove Cleveland and Cincinnati: historic downtown office buildings were available at acquisition prices that made residential conversion viable at rent levels the local market could actually support. Michigan’s historic tax credit program provided the public subsidy that closed the gap on buildings that otherwise would have sat vacant or been demolished. The combination of affordable acquisition and available incentive financing created the conditions for a conversion market that was active well before the pandemic created urgency elsewhere.

The result is a downtown residential inventory with genuine depth and character. Bedrock, founded by Dan Gilbert and headquartered in downtown Detroit, has been the largest single force behind this transformation, assembling a portfolio of historic downtown buildings and investing hundreds of millions of dollars in their restoration. Its projects anchor the core of downtown Detroit’s residential market in ways that ground-up luxury development in other cities cannot replicate. These are not anonymous towers. They are civic buildings with identity, and their conversion has preserved that identity while giving it new economic purpose.

The Conversion Projects That Define Downtown

Book Tower at 1265 Washington Boulevard

The most significant single adaptive reuse investment in downtown Detroit’s recent history is Bedrock’s $317 million restoration of the Book Tower at 1265 Washington Boulevard. Originally constructed in 1917 and one of the city’s most recognizable pre-war skyscrapers, the building had sat vacant for decades before Bedrock acquired and meticulously restored it. The completed project, which delivered in 2023, includes 229 residential units alongside ROOST Book Tower — a high-design extended-stay hospitality brand operated by Method Co. — and 85,000 square feet of retail and office space, two restaurants, a hotel lobby bar and lounge, a bakery, and a rooftop event space with panoramic views of the city. The building totals 677,895 square feet and is classified Class A, 4 Star.

At this scale of investment in a single historic building, Book Tower is the clearest signal of Bedrock’s long-term conviction in downtown Detroit’s residential market. The mixed-use program — combining residential, hospitality, food and beverage, and office in a single landmark building — establishes a template for density and activation that the surrounding blocks are still absorbing.

The Free Press Building at 321 W. Lafayette Boulevard

The Free Press Building at 321 W. Lafayette Boulevard, a 12-story Art Deco property completed in 1925, served as the headquarters of the Detroit Free Press for over 75 years. Its notable wall murals and limestone carvings — features that defined its civic identity for nearly a century — were preserved through Bedrock’s $69 million redevelopment, which converted the space into a mixed-use property with first-floor retail, office space on the second and third floors, and 105 residential apartments above. Following the newspaper’s relocation, the building had fallen into disrepair; the Bedrock restoration, completed in 2020, returned it to active use while preserving the architectural details that make it distinctive within the downtown streetscape. The building totals 302,400 square feet and is classified Class A, 4 Star.

Gabriel Houze at 305 Michigan Avenue

Originally constructed in 1940 as the Gabriel Richard Building, this 10-story property at the corner of Washington Boulevard and Michigan Avenue served as the headquarters of the Archdiocese of Detroit from the 1950s until 2014. Barbat Holdings converted it into Gabriel Houze, a $17 million project completed in 2020 that delivered 112 one-bedroom rental units showcasing Chicago School and Classical Revival architectural elements that survive in the building’s facade, lobby, and common areas. The building’s window line offers views of both the Detroit and Windsor skylines across the Detroit River, a distinctive amenity that is rare in the submarket. At 126,956 square feet and Class B, 3 Star, Gabriel Houze demonstrates that adaptive reuse in Detroit operates across a wide range of investment scales, not only the landmark-scale projects that attract the most attention.

The Pipeline: What’s Coming to Downtown

With the major Bedrock conversions now completed, the immediate new supply entering the downtown submarket is more modest. Yardi Matrix’s Q1 2026 data identifies two properties currently under construction in the downtown submarket, together adding 158 units to the market’s total of 11,383.

The Hive on Russell — 78 units by Develop Detroit — is expected to deliver in December 2026. The Reckmeyer — 80 units by BASCO of Michigan — is scheduled for January 2027. Beyond these near-term completions, the downtown pipeline holds 15 prospective properties representing 3,188 units in early planning stages, with The Palms Redevelopment, a planned 61-unit project, awaiting formal approval.

The contrast with the prior five-year cycle is striking. Downtown’s Lifestyle inventory grew 39% over the past five years, adding more than 1,100 units — the wave of conversion completions and new construction that now defines the submarket’s supply overhang. The current pipeline is a fraction of that volume, which is precisely the condition that supports gradual rent stabilization over the next two to three years.

What the Downtown Submarket Data Shows

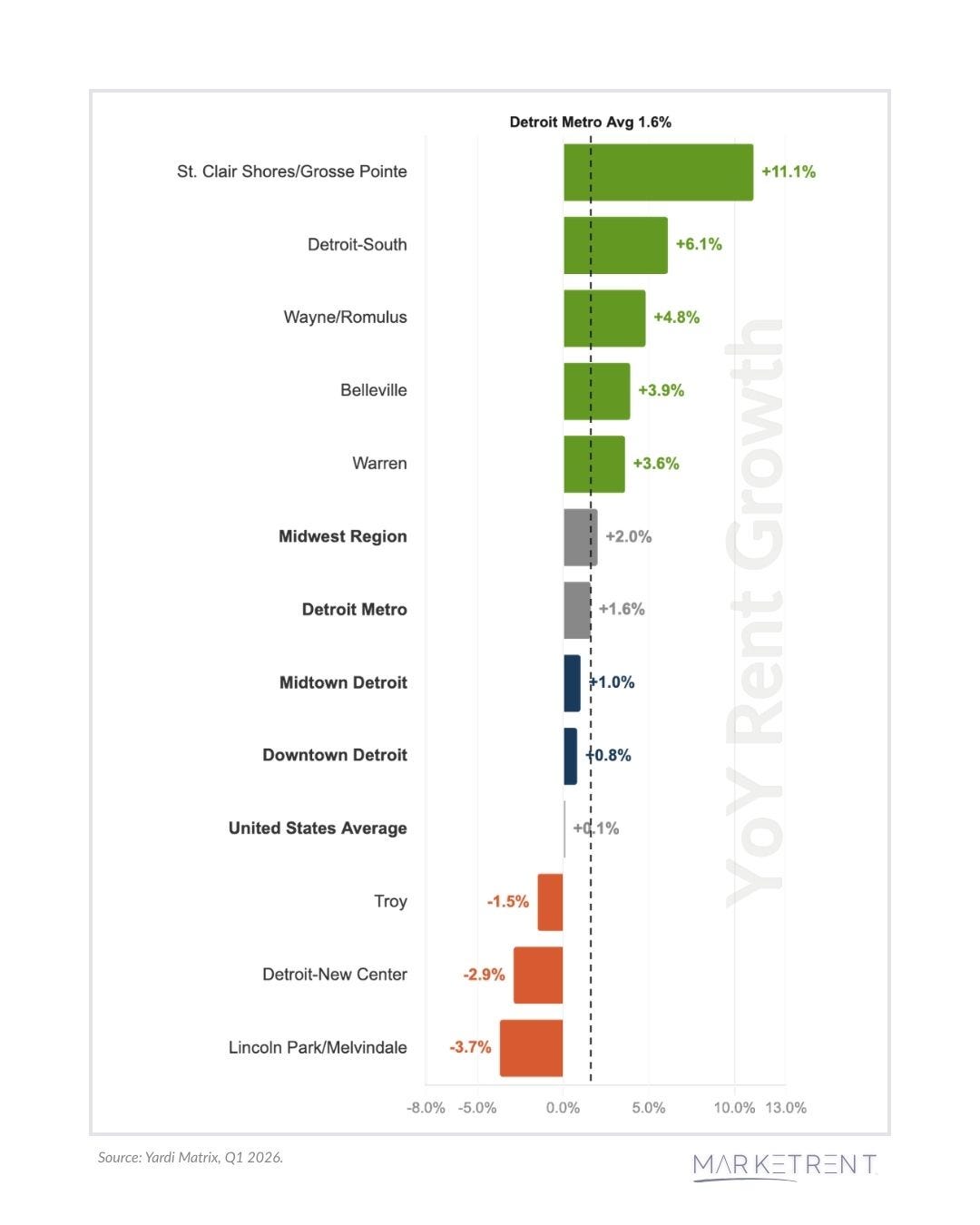

The pipeline context frames how to read the current submarket performance correctly. Downtown Detroit encompasses 62 properties with 11,383 units, average rents of $1,626 per month, and 92% occupancy as of Q1 2026 — ranking 42nd among 45 submarkets in occupancy and 31st in average rent.

Year-over-year rent growth stands at 0.8%, with one-bedroom units — the dominant unit type at 6,763 units — posting a 0.6% decline. Two-bedroom rents are essentially flat at 0.1% growth, reaching $1,925 per month. Three-bedroom units are the strongest performer at 2.9% growth and $2,678 per month, though the unit count is limited to 362.

This is a supply absorption dynamic, not a demand failure. Downtown added 1,124 units over the past five years — 11th highest of 31 submarkets with development activity — and the market is working through that delivery cycle. The building-class breakdown tells the nuanced story: the luxury tier, which absorbed the heaviest concentration of new supply, is facing the most pricing pressure. Mid-tier and workforce assets in the downtown core are performing more stably. That nuance is visible in the broader submarket context as well.

Looking forward, the data supports a measured recovery thesis. No new completions are projected for 2026 in the currently tracked pipeline. The two under-construction projects delivering in late 2026 and early 2027 represent a fraction of recent-cycle volumes. Rents are forecast to remain flat through year-end 2026, and occupancy is projected stable near 92% — setting the floor from which the submarket’s recovery will build as the prospective pipeline moves through approvals and market conditions determine what ultimately breaks ground.

Ready to go deeper on this market? Clarendon provides HUD Rent Comparability Studies, market studies, brokerage, and advisory services across major U.S. markets. To discuss your portfolio, visit clarendon.com/how-can-we-help.

What’s in the Full Market Brief

The MarketRent™ Detroit Market Brief covers the downtown adaptive reuse pipeline in depth — with individual project profiles including developer, unit mix, development cost, and construction status — alongside rent growth and vacancy analysis across the United States, Metro Detroit, Downtown Detroit, and Midtown Detroit submarkets by building class, and a review of the economic and institutional drivers shaping the market’s long-term trajectory. Access the full brief in the Market Reports section.

Policy Watch

HUD published revised FY 2026 Fair Market Rents (FR Doc. 2026-07741, effective May 21, 2026), updating FMRs for seven metropolitan areas based on new PHA survey data. Most Midwest and Northeast markets are unaffected. The notice also includes HUD’s responses to public comments on FMR methodology — covering the ACS data lag, the mandatory SAFMR program, and the reevaluation burden on PHAs — with direct implications for Section 8 renewal strategy.

Managing a portfolio of HUD-assisted properties? Clarendon’s Portfolio Program offers preferred terms, priority scheduling, and a single point of contact — reply or contact rfp@clarendon.com.

Related Resources

For more on Detroit’s broader market context, see The Motor City’s Second Act: Detroit Multifamily Market Intelligence. Explore the full Detroit development pipeline — including office-to-residential conversion profiles, construction status, and developer details — on the MarketRent™ interactive map. Next in this series: Midtown Detroit — institutional anchors, the M-1 Rail corridor, and the residential pipeline that is reshaping Detroit’s most strategically positioned submarket.

Podcast • Tools • Services • Archive • About • Contact

About: Clarendon is a trusted partner for government compliance and advisory solutions, specializing in HUD-compliant services: HUD RCS, appraisals, brokerage, inspections, facility support and strategic guidance for agencies, housing authorities and property owners nationwide.

© 2026 The Clarendon Group, Inc. All Rights Reserved. Disclosure