HUD Revises FY 2026 FMRs, Responds to Comments

Seven markets received revised FMRs effective May 21, 2026, alongside HUD's response to comments on the data lag in FMR methodology.

The Notice

On April 21, 2026, HUD published a revision to the FY2026 Fair Market Rents on the Federal Register, with revised FMRs taking effect May 21, 2026. The revisions apply to the Housing Choice Voucher Program, the Moderate Rehabilitation Single Room Occupancy Program, and other programs that rely on Section 8 FMRs. The revisions follow reevaluation requests submitted by Public Housing Agencies under HUD’s reevaluation request process, which allows PHAs to challenge published FMRs based on local rental market survey data they have commissioned.

HUD received 21 comments on the FY 2026 FMRs during the comment period, including 13 reevaluation requests covering 15 FMR areas. HUD determined that requests for 11 areas were valid; 4 requests did not meet HUD requirements. Of the 11 valid requests, 7 markets ultimately submitted the required local rental market survey data, and those 7 received revised FMRs in this notice.

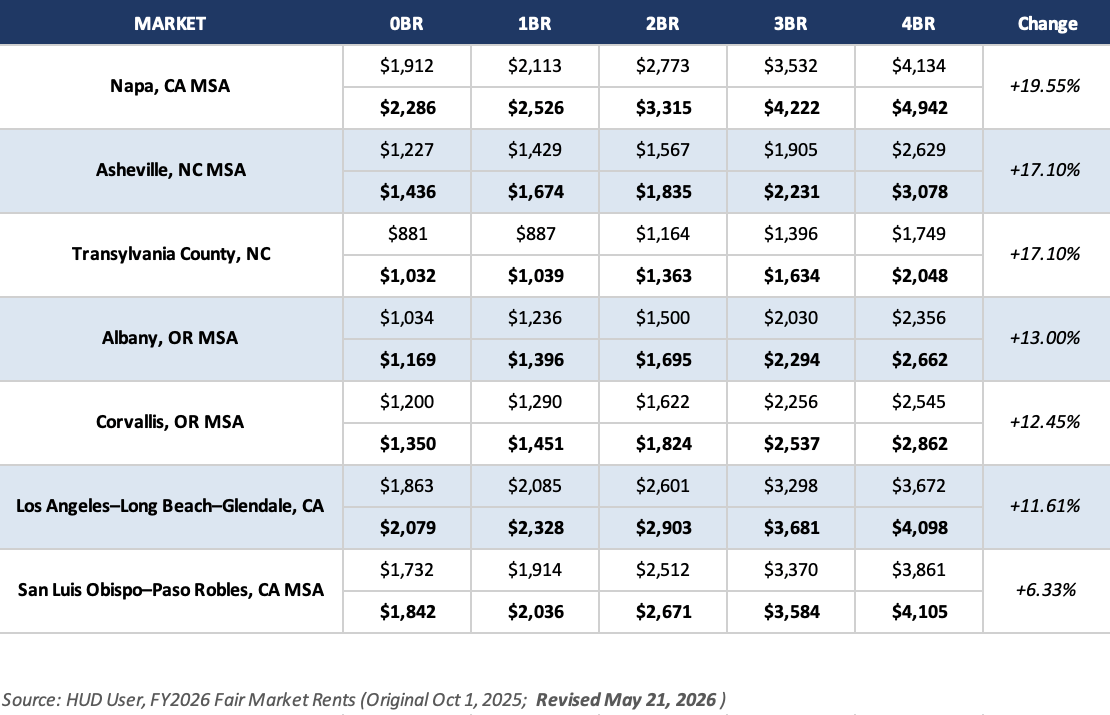

The seven affected markets are the Los Angeles–Long Beach–Glendale HUD Metro FMR Area in California, the Napa MSA in California, the San Luis Obispo–Paso Robles MSA in California, the Asheville HUD Metro FMR Area in North Carolina, Transylvania County in North Carolina, the Albany MSA in Oregon, and the Corvallis MSA in Oregon. For every other market in the country, the original FY2026 FMRs published October 1, 2025 remain in effect through September 30, 2026.

What Changed in the Seven Markets

Every revision moved upward, with magnitude ranging from 6.33% in San Luis Obispo–Paso Robles to 19.55% in Napa — the Los Angeles HMFA saw an 11.61% increase across all bedroom sizes.

The pattern across all seven markets is consistent. Every market increased, and every bedroom size within each market increased proportionally. The metro-level rent index resets reflect new PHA-conducted survey data submitted through the formal reevaluation process.

The revision updates the full FMR schedule (0–4 bedrooms) for seven markets where local Public Housing Agencies submitted new survey data that HUD determined warranted an adjustment. The revised FMRs reflect estimated 40th percentile rent levels trended to FY 2026, derived from PHA-conducted surveys. The Small Area Fair Market Rents (SAFMRs) for affected ZIP codes within these markets were updated in parallel as of May 21.

The Methodology Behind the Revisions

The magnitude of these revisions raises a methodological question worth examining. Why would a Federally-published FMR — based on the most recent American Community Survey data trended forward by HUD’s recent-mover and inflation factors — diverge from current market reality by 6% to 19% in select markets, requiring revision through PHA-conducted local surveys?

Three structural mechanisms drive the magnitude of these adjustments.

The base-year ACS data is two to three years old before it reaches the FMR calculation. FY 2026 FMRs use 2019–2023 5-year ACS data as the base year rents. The midpoint of that range is 2021. By the time the FY 2026 FMRs took effect on October 1, 2025, the underlying base-rent observation was already four years stale. HUD applies a recent-mover adjustment factor (using 2023 1-year ACS data) and an inflation trend factor to bring the figures forward, but in markets experiencing rapid rent growth — wildfire-affected Napa, post-Helene Asheville, and the California Coast tourism markets — the trend factor often understates actual rent appreciation.

The recent-mover adjustment factor is also lagged. The recent-mover adjustment is calculated by comparing 2023 1-year ACS recent-mover rents to the 2019–2023 5-year base rent. In high-volatility markets, by the time those 2023 figures are processed, the actual current market may have moved significantly further. The methodology has built-in correction for the data gap, but the correction itself is based on data that is two years old by the effective date.

PHA-conducted local surveys can capture conditions ACS cannot. When a PHA commissions an independent rental survey using HUD-approved survey protocols, the resulting data reflects market conditions much closer to the survey date — typically within 3 to 6 months. When that survey produces a 40th percentile two-bedroom rent meaningfully different from the ACS-derived figure, HUD will revise the FMR. The 19.55% Napa revision and the 11.61% Los Angeles revision tell us something specific: the gap between the ACS-derived FMR and current market reality, in these specific markets, was substantial enough that a properly conducted local survey produced a fundamentally different answer. That is not a quirk of the methodology — that is the methodology working as designed when local survey data is available and is more current than ACS data.

Case Study: The Los Angeles HMFA

The Los Angeles revision provides a useful look at how mid-year reevaluations flow through to Small Area Fair Market Rent data at the ZIP code level. The Los Angeles HMFA contains 474 ZIP codes. Of those, 460 ZIP codes — or 97% — saw a SAFMR increase. Fourteen ZIP codes held steady at original FY2026 levels. Zero ZIP codes decreased. Among the ZIP codes that changed, 434 — or 92% of those affected — landed within a tight band of 10 to 12.5%. The median two-bedroom SAFMR change was $300 per month.

The 14 unchanged ZIP codes span a range of submarket profiles, some are fringe exurban areas and others are in-metro locations. The common thread is not geography or rent tier. It is that the original SAFMRs for those ZIP codes already aligned with neighborhood-level market rents. For Section 8 owners with properties in the affected Los Angeles ZIP codes, the revised SAFMRs increase the 150% threshold ceiling correspondingly.

The Public Comment Response

The April 21 Federal Register notice also includes HUD’s response to the 21 public comments received during the FY 2026 FMR comment period (initially opened with the August 22, 2025 publication and extended via the September 19, 2025 corrected notice). The comments raised structural questions about the data lag between ACS observation periods and FMR effective dates, the responsiveness of the recent-mover adjustment factor to rapidly changing markets, and the geographic granularity of FMR areas relative to actual rental sub-markets.

HUD’s response acknowledges the data-lag concerns and notes that the reevaluation request process exists specifically to address situations where local data demonstrates that published FMRs understate current rent levels. The notice does not commit to methodology changes for FY 2027 but does signal that HUD is studying the comment record for potential improvements in future fiscal years.

On FMR accuracy and data lag, one commenter stated that FMRs in fast-moving markets are perpetually behind the curve due to the built-in lag in American Community Survey data, and requested semi-annual or quarterly FMR updates in high-volatility markets. HUD responded that ACS data remains the only nationwide rent dataset with statutory advantages sufficient to compel responses and generate statistically representative results. HUD stated that proprietary rent data cannot serve as the sole basis for FMR calculations because such sources do not consistently produce the 40th percentile recent-mover estimate required by regulation. HUD indicated it will evaluate the feasibility of more frequent updates alongside available resources but made no commitment to change the current annual schedule.

On the reevaluation process, several commenters questioned the equity of requiring PHAs to bear the full cost of independent market surveys when pursuing FMR reevaluations, noting that survey costs come at the expense of voucher holders and core PHA functions. Commenters requested a HUD grant program to fund reevaluations, acceptance of private data where appropriate, and proactive HUD identification of areas warranting reevaluation. HUD responded that local rental market survey costs are eligible expenses from Housing Choice Voucher administrative fees or administrative fee reserves. HUD noted that its existing private data sources cannot serve as the sole basis for FMR calculations and that its ability to fund PHA surveys is subject to appropriations. No new funding mechanism was announced.

On mandatory Small Area FMRs, one commenter requested elimination of mandatory SAFMRs, arguing that PHAs better understand their specific markets. HUD declined the request and confirmed that mandatory SAFMRs remain in effect across all 65 designated metropolitan areas. The 150% SAFMR Threshold Test for Section 8 Rent Comparability Study submissions is unchanged.

The pattern across HUD’s responses is consistent. Acknowledgment of the underlying critiques, defense of the current framework, and no near-term structural changes. The responses document that FMRs lag actual market conditions, and that the reevaluation pathway, while open, remains PHA-dependent and resource-intensive.

What This Means for the Broader Audience

The seven-market revision exists because seven PHAs submitted requests with new survey data. The precedent now exists for owners and PHAs in other markets where the original FY2026 FMRs may be misaligned with current rent reality — particularly in markets with active development pipelines, significant rent growth since the FMR survey window, or supply constraints.

For Section 8 owners and contract administrators, the lesson is structural: in any market that has experienced meaningful rent growth between 2021 and 2025, the published FMR likely understates what current market rents support. The FMR revision process is one mechanism for correcting that gap. A property-specific Rent Comparability Study, conducted with current market comparables, is the other.

For the SAFMR process specifically, the metro-level FMR revision flows through to every ZIP code within that metro. Because the SAFMR for a ZIP code is calculated as a ratio of that ZIP’s median rent to the metro median rent, applied to the metro FMR, when the metro FMR is revised upward, every SAFMR within that metro is revised upward proportionally. For RCS practitioners, this means the 150% SAFMR Threshold Test for any property in the affected ZIP codes has effectively just moved.

For owners in the seven affected markets, timing considerations matter. An RCS signed by the owner’s appraiser on or after May 21, 2026 will reference the revised FMRs.

Managing a portfolio of HUD-assisted properties? Clarendon’s Portfolio Program offers preferred terms, priority scheduling, and a single point of contact — reply or contact rfp@clarendon.com.

Related Resources

For background on SAFMR methodology and the 150% Threshold Test, see Four Markets. Four Different Stories: What FY 2026 SAFMRs Reveal. For a deeper look at how PHA survey data interacts with the FMR system, see HUD's FMR Reevaluation FAQs.

Podcast • Tools • Services • Archive • About • Contact

About: Clarendon is a trusted partner for government compliance and advisory solutions, specializing in HUD-compliant services: HUD RCS, appraisals, brokerage, inspections, facility support and strategic guidance for agencies, housing authorities and property owners nationwide.

© 2026 The Clarendon Group, Inc. All Rights Reserved. Disclosure