The Midtown Detroit Thesis

Wayne State University, Henry Ford Health, and the Woodward Corridor — the institutional infrastructure behind Midtown Detroit's residential market.

This is the third article in MarketRent™’s Detroit series. The city-level overview was published in The Motor City’s Second Act. The Downtown conversion pipeline was covered in The Conversion Pipeline That Remade the Core. This piece covers Midtown specifically — the institutional anchors that drive its residential demand, the M-1 Rail corridor that connects it, and the development pipeline that is reshaping the most strategically positioned submarket in the metro.

One mile north of Downtown Detroit, a different residential investment thesis is playing out.

Midtown sits along the Woodward Corridor between the central business district and the New Center, anchored by Wayne State University and Henry Ford Health on its eastern flank, the Detroit Institute of Arts and the Detroit Public Library at its center, and the QLine streetcar threading through it all. The institutional infrastructure is dense, durable, and structurally different from anything else in the metro.

That institutional density translates directly into residential demand. Midtown’s renter base — students, hospital staff, faculty, healthcare professionals, museum employees — is anchored to physical locations that don’t relocate, don’t downsize, and don’t work from home. It’s the kind of demand profile that supports development through cycles where other submarkets stall.

The data shows what that demand profile produces.

The Institutional Demand Layer

Wayne State University enrolls roughly 24,000 students across its Midtown campus, with concentration of housing demand for both the student population and the faculty, staff, and graduate students who prefer to live within walking or QLine distance of campus. Henry Ford Health employs more than 33,000 people across the Detroit health system, with its main campus and several specialty centers concentrated along the Woodward Corridor in Midtown and the adjacent New Center submarket.

Together, these two institutions generate a base layer of approximately 57,000 daily destinations within the submarket — workers, students, patients, and visitors whose presence in Midtown is structural rather than discretionary. That demand layer is supplemented by the Detroit Medical Center campus to the east, the Detroit Institute of Arts and the Detroit Public Library at the cultural anchor of the submarket, and the smaller institutional employers (Cranbrook Schools’ Detroit operations, the Michigan Science Center, the Charles H. Wright Museum of African American History) that round out the institutional ecosystem.

For residential investors, this profile matters because institutional demand is fundamentally different from market-rate demand. It is less elastic with respect to rent. Less volatile across economic cycles. Less likely to disappear when the labor market cools or when consumer discretionary spending contracts. It is also slow to grow — institutional employers don’t add 5,000 jobs in a quarter — but the base it provides is durable in a way that few residential submarkets can replicate.

The M-1 Rail and the Corridor That Connects It

The QLine, formally the M-1 Rail, runs 3.3 miles along Woodward Avenue from Larned Street downtown north to Grand Boulevard in the New Center. It opened in 2017, was acquired by SMART (Detroit’s regional transit authority) in 2024, and is now operated as part of the regional transit network with extended hours and integrated fare structure with regional bus service.

For Midtown specifically, the QLine functions as the spine of the submarket’s residential geography. Properties within walking distance of QLine stops command rental premiums that show up clearly in the building-class data. The streetcar’s 12 stops connect every major Midtown employer, every cultural institution, and every recently completed or under-construction residential development along the corridor. It is not a comprehensive transit system, but for the residential demand it serves, it is the relevant one.

What the Midtown Submarket Data Shows

Midtown Detroit encompasses 61 properties with 8,250 units, average rents of $1,438 per month, and 92.3% occupancy as of Q1 2026 as reported by Yardi Matrix. Year-over-year rent growth stands at 1.0% — modestly below the metro average of 1.6%, but the headline number understates what is actually happening in the submarket.

The Lifestyle tier — the building class most exposed to new supply — is performing strongly at $1,581 per month and 3.1% year-over-year growth, ranking the submarket third among all Detroit metro submarkets in Lifestyle rent growth. One-bedroom Lifestyle rents specifically posted 2.5% growth, reaching $1,310 per month. These figures contradict the assumption that the metro-wide Lifestyle pricing pressure visible in Downtown applies uniformly across the metro. Midtown’s Lifestyle tier is performing as if the metro narrative does not apply to it — because it largely does not.

The five-year inventory growth context explains why. Between 2021 and 2025, Midtown’s Lifestyle inventory grew 34.83% — significant volume, but absorbed against a demand layer that grew with it. The 2026–2027 forward Lifestyle pipeline shows N/A. There is no new Lifestyle supply scheduled to enter the submarket through year-end 2027. The Lifestyle wave already happened in Midtown. The supply absorption is complete. What developers are building now is something else entirely.

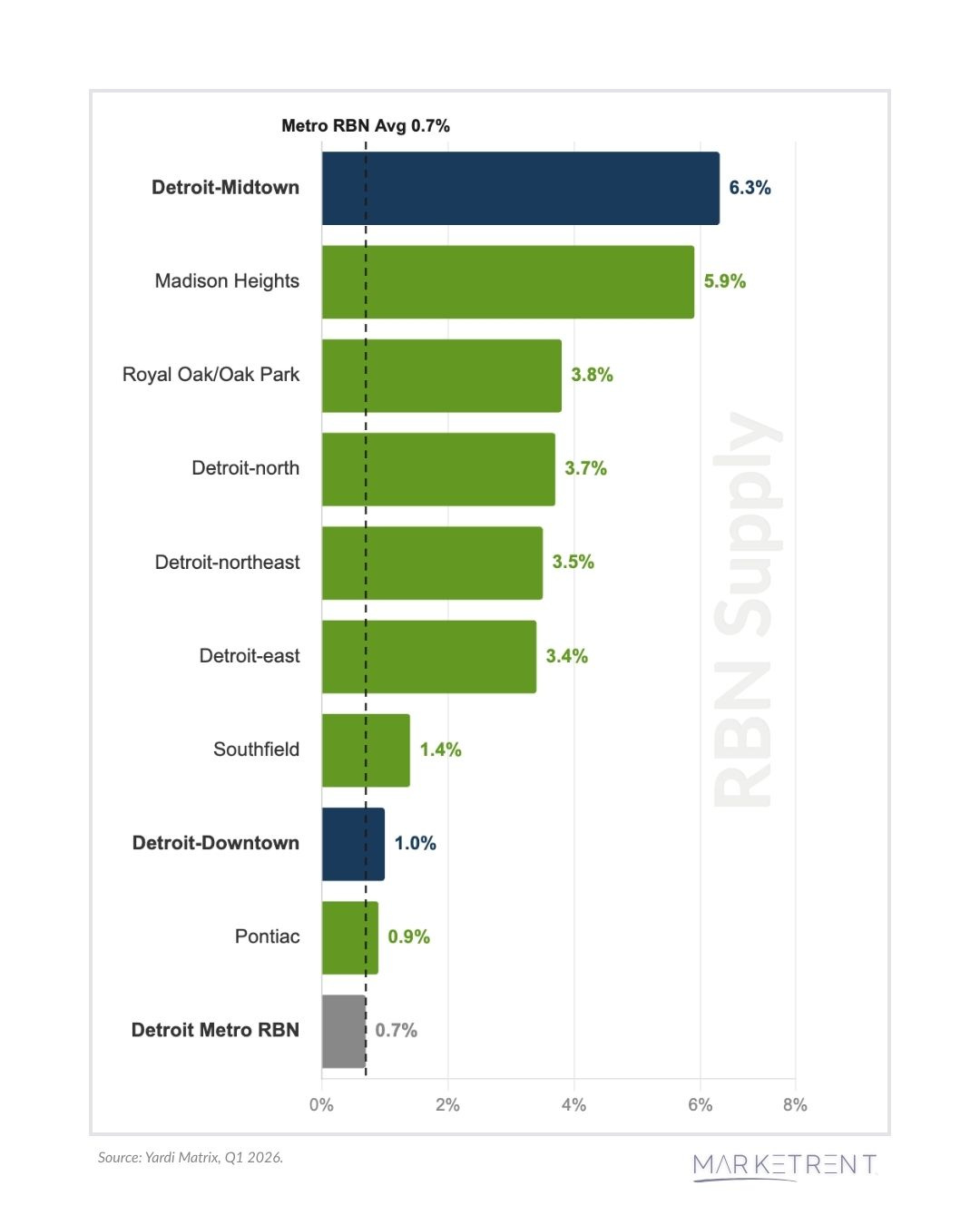

The RBN Pipeline: Where Midtown Is Building Next

Midtown’s projected Renters-by-Necessity (RBN) completions over the 12 months ending February 2027 stand at 6.3% of inventory — nearly nine times the Detroit metro RBN average of 0.7%. The submarket is now the strongest workforce-housing pipeline in the metro by a meaningful margin, and the asset class shift signals where developers see the next demand layer forming.

The RBN tier — the B-through-D building classes serving renters whose housing choices are driven by economic necessity rather than lifestyle preference — is the asset class most directly comparable to Project-Based Section 8 housing. For Midtown, the institutional demand layer makes RBN development viable: hospital staff, university support employees, cultural institution workers, and graduate students all generate demand at rent levels that workforce housing serves. The pipeline reflects this. Nearly the entire forward-looking Midtown development pipeline is RBN.

Brush Watson at 444 Watson Street

The largest project in the current Midtown pipeline is Brush Watson, a 310-unit multi-phased RBN development by American Community Developers with a $45 million development cost and a January 2027 completion target. The project, located on Watson Street in the heart of Midtown, has been in active development since 2021. Its scale — over half of the entire Midtown under-construction unit count — makes it the single most consequential addition to the submarket’s residential inventory in the current cycle.

4401 Rosa Parks Boulevard

4401 Rosa Parks is a 60-unit project by Cinnaire, a Michigan-based community development financial institution focused on affordable housing investments. Construction started October 2025 with a December 2026 completion target. The project is a smaller-scale RBN addition oriented toward the lower-income demand segment that the institutional ecosystem also serves.

The Mid at 3750 Woodward Avenue

The Mid is a planned 370-unit project by Real Estate Interests with a Woodward Avenue address that places it directly on the QLine corridor. Submitted October 2019 for entitlement review, the project remains in the planned-but-not-yet-broken-ground phase. When delivered, it will be one of the larger residential additions to the corridor and will solidify the QLine’s residential anchor function.

The American at 408 Temple Street

The American is a 149-unit planned project by Olympia Development of Michigan, the residential development arm of Ilitch Holdings. Submitted in January 2023, the project sits within the broader District Detroit redevelopment program that has been transforming the Cass Corridor and the Brush Park / District Detroit interface for the past decade.

What This Means for Owners and Investors

The Midtown story is structurally different from the Downtown story. Where Downtown is working through a Lifestyle absorption cycle from a recent supply wave, Midtown’s Lifestyle absorption is complete and the next development cycle is workforce-tier. For owners holding existing Midtown assets, the institutional demand layer provides a stability floor that few other Detroit submarkets can match. For investors evaluating new acquisitions, the asset class composition of the forward pipeline matters — Midtown’s competitive set in 2027 will be heavier on RBN supply than it has been in the recent past.

The competitive implications extend across asset classes. New workforce-housing supply at this scale in a single submarket can shift rent comparability dynamics over the medium term. The 6.3% pipeline doesn’t compress rents immediately, but as units deliver in 2026 and 2027, the supply layer will register in market studies and rent comparability analyses for properties in the surrounding ZIP codes. Owners evaluating Midtown acquisitions in 2027 or planning capital improvements to existing assets should be monitoring the pipeline as a leading indicator for how the competitive set will look when those investments come to market.

Ready to go deeper on this market? Clarendon provides HUD Rent Comparability Studies, market studies, brokerage, and advisory services across major U.S. markets. To discuss your portfolio, visit clarendon.com/how-can-we-help.

What’s in the Full Market Brief

The MarketRent™ Detroit Market Brief covers Midtown's institutional ecosystem and forward development pipeline in depth — with individual project profiles including developer, unit mix, development cost, and construction status — alongside rent growth and vacancy analysis across the United States, Metro Detroit, Downtown Detroit, and Midtown Detroit submarkets by building class, and a review of the economic and institutional drivers shaping the market's long-term trajectory. Access the full brief in the Market Reports section.

Policy Watch

HUD published revised FY 2026 Fair Market Rents (FR Doc. 2026-07741, effective May 21, 2026), updating FMRs for seven metropolitan areas based on new PHA survey data. Most Midwest and Northeast markets are unaffected. The notice also includes HUD’s responses to public comments on FMR methodology — covering the ACS data lag, the mandatory SAFMR program, and the reevaluation burden on PHAs — with direct implications for Section 8 renewal strategy.

Managing a portfolio of HUD-assisted properties? Clarendon’s Portfolio Program offers preferred terms, priority scheduling, and a single point of contact — reply or contact rfp@clarendon.com.

Related Resources

For more on Detroit’s broader market context, see The Motor City’s Second Act: Detroit Multifamily Market Intelligence. Explore the full Detroit development pipeline — including office-to-residential conversion profiles, construction status, and developer details — on the MarketRent™ interactive map.

Podcast • Tools • Services • Archive • About • Contact

About: Clarendon is a trusted partner for government compliance and advisory solutions, specializing in HUD-compliant services: HUD RCS, appraisals, brokerage, inspections, facility support and strategic guidance for agencies, housing authorities and property owners nationwide.

© 2026 The Clarendon Group, Inc. All Rights Reserved. Disclosure